|

Formulas:

Holding period yield

Money market yield

Effective annual yield

Holding period yield

Bond equivalent yield

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Exercise Problems:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

1. A project offers the following incremental after-tax cash flow. The discount rate of the project is 10%:

The NPV and IRR of the project is closest to: NPV IRR A. 31.2 12.0% B. 240 10.0% C. 31.2 10.0%

|

|

Ans: A; Use calculator:

NPV=31.2

IRR=12.0%

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2. When considering two mutually exclusive capital budgeting projects with conflicting rankings, the most appropriate conclusion is to choose the project with the: A. Shorter payback. B. Higher NPV. C. Higher IRR.

|

|

Ans: B; since the NPV of an investment represents the expected addition to shareholder wealth from an investment, and we take the maximization of shareholder wealth to be a basic financial objective of a company. A is incorrect; Payback period refers to the period of time for the return on an investment to “repay” the sum of the original investment. The shortcoming is ignoring the cash flow after the payback period. C is incorrect; IRR rules may be meaningless when the scale of projects or timing of cash flows is different. Also IRR calculation furthermore assumes reinvestment at the IRR, which always cannot be achieved.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

3. Nan Chen purchases 100 shares of Bao Capital’s stock at a price of $40 on March 1st, 2012, and then sells them on $43 on August 1st, 2012. During the year of 2012, Bao Capital paid dividends of $0.5 per share on January 1st and July 1st. the holding period return on the investment is closest to: A. 7.50% B. 8.75% C. 10.00%

|

|

Ans: B; Holding

period return determines the return that an investor will earn by holding the

instrument to maturity; as used here, this measure refers to an unannualized

rate of return. The formula to calculate holding

period return is as below: In this problem P0=40, P1=43, and D1= 0.5, so HPY=8.75%

A is incorrect; since it ignores the dividend.

C is incorrect; though Bao Capital paid dividend twice in 2012, but there was only once during Nan held the shares, so dividend is $0.5, not $1.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

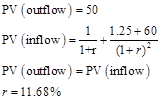

4. Junyun Lu purchases one share of stock for $50. Exactly one year later, the company pays a dividend of $1 per share. This is followed by one more annual dividends of $1.25. And then she sells the share for $60. The money-weighted rate of return on this investment is closest to: A. 24.50% B. 20.00% C. 11.68% |

|

Ans: C ; The money-weighted rate of return is the IRR calculated using periodic cash flow into and out of an account and is the discount rate that makes the PV of cash inflows equal to the PV of cash outflows. In this problem:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

5. An analyst gathers the following information about the performance of a portfolio:

The portfolio’s annual time-weighted rate of return is closest to: A. 8% B. 27% C. 32%

|

|

Ans: C : The time-weighted rate of return measures compound growth. It is the rate at which $1 compounds over a specified performance horizon. In this problem:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

6. On 1 January 2012, Yang Liu purchases 100 shares of stock for $10 a share. On 1 March 2012, she purchases 100 more shares of the sane stock for $12.5 a share. On 1 June 2012, she sells all 200 shares of the stock for $15 a share. The internal rate of return for this investment is best described as an example of a: A. Geometric mean return B. Time-weighted rate of return C. Money-weighted rate of return

|

|

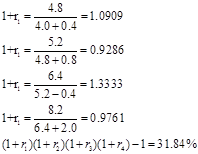

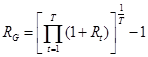

Ans: C; since The money-weighted rate of return is the IRR calculated using periodic cash flow into and out of an account and is the discount rate that makes the PV of cash inflows equal to the PV of cash outflows. A is incorrect; given a time series of holding period returns Rt, the geometric mean return over the time period spanned by the returns R1 to RT is

B is incorrect; The time-weighted rate of return measures compound growth. It is the rate at which $1 compounds over a specified performance horizon.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

7. The dollar discount on a U.S. Treasury bill with 182 days until maturity is $20. The face value of the bill is $1,000. The holding period yield and the bank discount yield of the bill is closest to: HPY rBD A. 2.04% 4.01% B. 2.04% 3.96% C. 4.10% 4.01% |

|

Ans: B; Holding

period return determines the return that an investor will earn by holding the

instrument to maturity; as used here, this measure refers to an unannualized

rate of return. In this problem, no dividend paid

during the holding period, so: Bank discount basis is a quoting convention that annualizes, based on a 360-day year, the discount as a percentage of face value.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

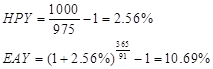

8. A 91-day U.S. Treasury bill has a face value of $1,000 and currently sells for $975. Which of the following yields is most likely the highest? A. Bank discount yield B. Money market yield C. Effective annual yield |

|

Ans: C; effective

annual yield is calculated as below: In this problem,

A is incorrect;

B is incorrect; money market yield (also known as the CD equivalent yield) makes the quoted yield on a T-bill comparable to yield quotations on interest-bearing money-market instruments that pay interest on a 360-day basis.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

9. The bond-equivalent yield for a semi-annual pay bonds is most likely: A. Equal to the effective annual yield B. More than the effective annual yield C. Equal to double the semi-annual yield to maturity

|

|

Ans: C; bond-equivalent yield calculated ignoring compounding, annualizing a semiannual yield by doubling is putting the yield on a bond-equivalent basis. |

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

10. Victor Chow, CFA, held a 10% coupon bond for six months while the following results: Initial price: 100% of par End of holding period price: 97% of par The holding period yield and Effective annual yield of the bond is closest to: HPY EAY A. 7.00% 10.00% B. 7.00% 14.49% C. 14.00% 14.49% |

|

Ans: B; Holding

period return determines the return that an investor will earn by holding the

instrument to maturity; as used here, this measure refers to an unannualized

rate of return. The formula to calculate holding

period return is as below: In this problem, assume par value is 100, P0=100, P1=97, and D1= 10, so HPY=7%

effective

annual yield is calculated as below: In this problem,

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

移动客户端:iPhone版 iPad版 安卓版,

助你随时随地、离线学习!